Executive summary

Renewable energy still attracts a growing share of investment in new electricity generation capacity. Some US$370 billion is forecast worldwide in 2020, up 50 percent on 2016. Little of this investment is currently slated for the Gulf Cooperation Council (GCC)1 states. The GCC is falling behind developed countries such as Germany, and developing economies such as Chile, Mexico, Morocco, and South Africa.

Although structural and institutional challenges for renewables have led to underinvestment, the GCC has several factors that make rapid deployment of renewables an attractive opportunity. These include plentiful, high-yield renewable resources; an natural gas shortage; and an established independent power plant (IPP) model, which makes cheap, long-term project finance available and can attract the necessary private and foreign investors.

Capitalizing on that opportunity requires a considerable financial and policy commitment. GCC governments must avoid a short-term, haphazard approach that will result in an inefficient supply mix or renewables plants disconnected from national energy strategy. To avoid such risks, GCC governments should take six critical actions. These create a policy framework that supports open, transparent, and competitive investments in renewables generation capacity, helping governments minimize costs and achieve their national economic development objectives:

- Set ambitious and realistic renewable energy targets that are grounded in a comprehensive and integrated national energy plan

- Clarify the national energy governance framework and define institutional roles and accountabilities

- Reform the current fossil fuel and energy subsidies regime and reallocate financial resources

- Broaden the range of financing instruments available to renewables

- Unify regional standards to aggregate demand for equipment and increase transparency and comparability across projects

- Build the capabilities of policymaking and regulatory authorities.

Great potential for the GCC

The GCC countries are an ideal market for renewable energy deployment. Indeed, the case for rapid deployment of renewable energy is actually stronger in the GCC region than in many other developing economies. Three fundamental features of the region’s energy supply system explain this potential:

Ample high-yield renewable resources

Located in the heart of the global sunbelt, GCC countries have some of the highest solar exposures in the world. Solar power plants in the region can expect 1,750 to 1,930 hours of full-load operation per year. Contrast this with solar plants in Germany, which register, on average, only 940 hours of full-load operation per year. A solar-photovoltaic panel in a GCC country produces twice as much output as it would in Germany or any similar European country.

Furthermore, the output of a solar power plant in the GCC lines up with daily and seasonal variations in demand. Air conditioning demand, which drives peak electricity consumption in GCC countries, rises and falls in tandem with the output of solar power plants. In countries with colder climates, by contrast, the demand for electricity is typically highest on cold and dark winter days, when solar plant outputs are lowest. As a result, renewables should improve the overall efficiency of the GCC electricity system.

The region also has areas with high-velocity wind resources. Parts of Kuwait, Oman, and Saudi Arabia in particular are suitable for onshore wind farms.

An enduring natural gas shortage

GCC countries are major consumers of energy in their own right, with a rapidly growing demand for electricity. At the same time, demand for hydrocarbons as fuel and as feedstock is increasing because of the expansion of energy-intensive industrial activities. Although liquid hydrocarbon production capacity remains largely in surplus, the region as a whole faces an enduring gas shortage that is compelling it to develop increasingly remote and technically challenging gas resources. The uncertainty in the timing, volumes, and cost of new gas supplies forces some GCC countries to burn expensive crude oil and liquid fuels to generate electrical power.

Using renewables would reduce the imports of expensive refined liquid hydrocarbon products and free up oil production capacity to enhance the region’s position as a major exporter and swing producer for the world. Similarly, a greater reliance on renewables would ensure that natural gas is allocated to the applications and end users that create the most value for national economies.

A bankable model for private investment

The availability of cheap long-term project finance under the IPP contractual model allows the GCC to attract the necessary private and foreign investments into power generation. The IPP model of privately financed power generation assets is well-established in the GCC, with a track record of stability and success that spans more than two decades. The availability of cheap long-term project finance under a well-established IPP contractual model makes the GCC an eminently suitable market for attracting the necessary private and foreign investments in power generation infrastructure.

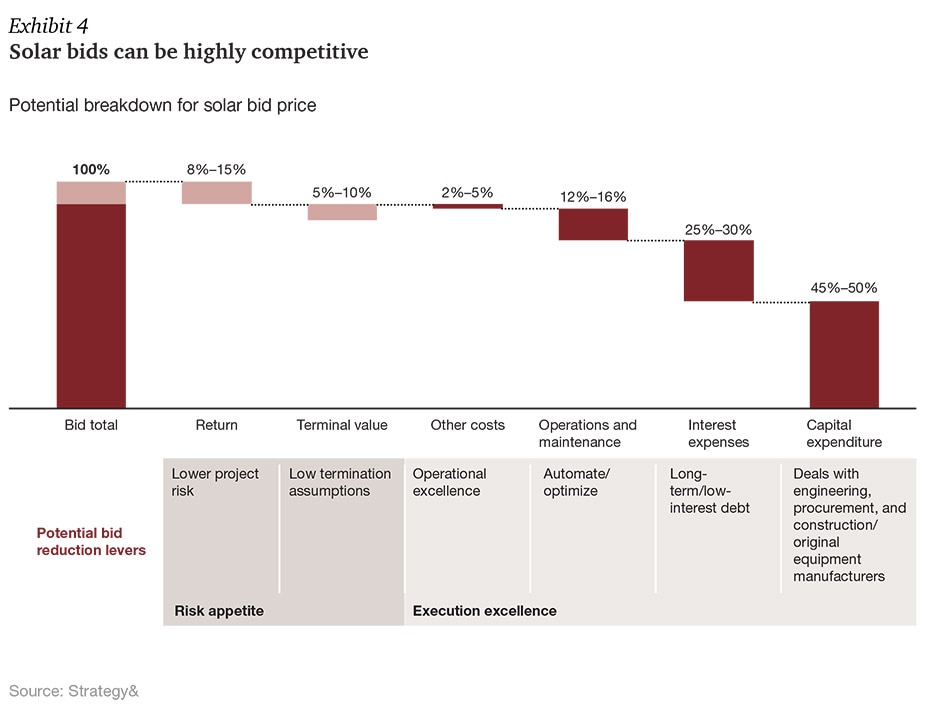

The IPP model is a pure commercial credit product, which is why it fits well with renewable energy. The cash flow profile for a renewables project differs fundamentally from a fuel-consuming, conventional power project: the economics of a renewables project are almost exclusively determined by one-time, up-front costs with negligible ongoing operations and maintenance (O&M) costs. The GCC has several best-in-class project developers that understand the characteristics of renewables financing. These developers are able to combine offtaker credit with an understanding of the technology and market, and they have the appetite and knack for turning long-term risks into bespoke credit products for commercial lenders (see Exhibit 4).

Six critical actions for GCC governments

GCC governments must act urgently to lead the inevitable transition to a modern, renewables-based energy system. Today’s fiscal challenges in particular leave little room for continued indecisiveness and postponed reforms. In this uncertain economic environment, GCC countries will not have the luxury of reversing poor infrastructure investment decisions. They therefore need to assess carefully the long-term implications of the path they choose before embarking on it. Excessive focus on the short term could lead to poor decisions, which will have ramifications for decades to come.

Other developing countries have already successfully applied a suite of policies and initiatives that GCC policymakers can exploit. International experience points to six critical actions that can be adapted to the specific circumstances of each GCC country.

1. Set ambitious, realistic targets grounded in a comprehensive and integrated national energy plan

Ambitious yet realistic targets provide critical signals to private developers and investors that allow them to plan for the long term and arrange the necessary financing and bidding consortia well in advance. Furthermore, successful and timely procurement of generation capacity according to an announced schedule builds private-sector confidence and widens the pool of accessible financial resources.

Governments should ground their renewables targets in a comprehensive national energy plan that optimizes the entire value chain, from upstream primary energy sources to downstream end-users. The best energy mix is based on holistic systems of technologies that satisfy daily and seasonal demand on a lowest-cost basis, not on an isolated or static assessment of individual technologies and their levelized cost of energy (as can sometimes occur). Analyses should capture the full cost of electricity supply to an end-user, including system integration costs such as backup capacity, increased intermittency balancing requirements, and T&D network reinforcement. Furthermore, the plan should consider all potential options, including renewables, imports of coal, piped natural gas, and liquid natural gas.

2. Clarify the national energy governance framework and define institutional roles and accountabilities

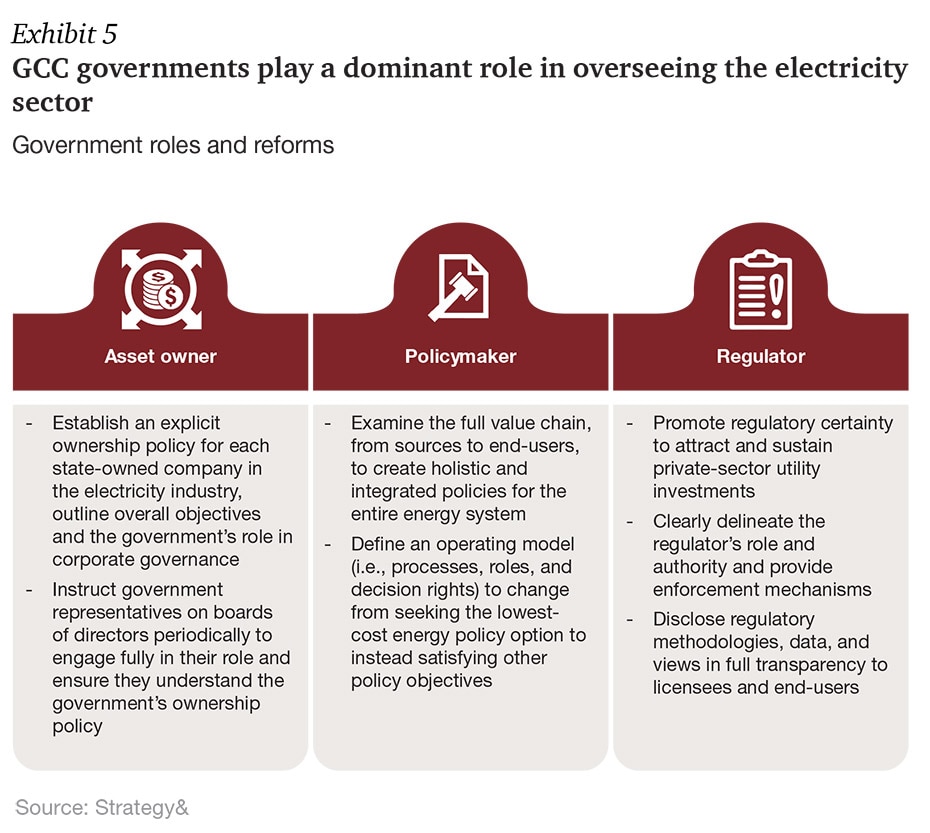

Ensuring the long-term health of the electricity sector and enhancing its attractiveness to private investors requires a clear separation between the government’s functions as an asset owner, policymaker, and regulator. Such a separation is important to allow the private sector to thrive under the centrally planned system of electricity service provision and planning that will likely remain intact in the GCC for decades to come (see Exhibit 5). Separating these roles will create checks and balances that make the national electricity industry’s decision-making processes transparent, participatory, accountable to the public interest, and nondiscriminatory.

3. Reform fossil fuel and energy subsidies and reallocate financial resources

The long-term financial viability of the electrical power industry as a whole, and of renewables in particular, hinges on phasing out subsidies and reforming electricity tariffs. These need to reflect the full economic cost of generating and delivering a kilowatt-hour. Quantifying the right level of support that GCC governments should provide to electrical utilities presents significant challenges. As a starting point, transparent data on fossil fuel subsidies will raise awareness about their magnitude. Such information can encourage an informed debate on whether the subsidy represents an economically efficient allocation of resources. Full clarity on the subsidy regime will occur only when all forms of direct and indirect subsidies are concentrated into direct supplements to the tariffs paid by end-users through a predictable and systematic support mechanism.

We estimate that fossil fuel consumption subsidies in the GCC, inclusive of power generation fuel supply, amounted to $30 billion in 2016, matching Germany’s renewable energy subsidies in the same year. Reallocating merely a fraction of GCC subsidies from fossil fuels to support private-sector-led development of renewable energy grid-integration investments could create tremendous value for governments, investors, and electricity consumers.

4. Broaden the range of financing instruments available

Credit product innovations can help meet the requirements of the renewables market and increase the liquidity and competitive financing available for new projects. Public utilities and private developers need improved access to corporate bond and sukuk markets (bonds that comply with Islamic law). Despite often having higher transaction costs, longer lead times, and less flexibility than commercial loans, bonds typically offer longer terms, lower interest rates, and access to a considerably larger funding pool.

GCC countries should also consider creating the necessary legal instruments to allocate risk optimally to the partner most capable of managing it at each phase of the project. Developers and other investors can thereby variably allocate risk and ownership levels based on predefined milestones and/or yield thresholds. Such instruments include partnership flips, sale and leaseback, and securitizing future IPP cash flows into publicly traded yield companies.

Finally, introducing derivatives into GCC capital markets could support risk management and increase market liquidity for renewables IPP development. Such financial instruments include interest rate swaps, government bond forwards, and currency exchange swaps.

5. Unify regional standards

The lack of unified renewables standards creates unnecessary trade and investment barriers. Establishing clear standards for wind and, to a lesser degree, solar would reduce these barriers among GCC countries and across the broader Middle East region. Already the solar-photovoltaic industry features standard, modular technologies with limited differences in technical specifications and standards across countries. By contrast, the wind-energy sector allows nationally distinct technical specifications and certification standards for wind-turbine components.

6. Build policymaking and regulatory capabilities

The large-scale deployment of renewable energy through privately led initiatives requires a level of capabilities that is beyond that currently possessed by most ministries. To work together effectively, policymakers, regulators, owners, and operators can upgrade their capabilities in technical and economic analysis, forecasting, simulation, communication, and management. Although Oman, Saudi Arabia, and the emirates of Abu Dhabi and Dubai in the United Arab Emirates have made notable progress in sourcing, developing, and retaining the required skills, such policymaking and regulatory oversight of the electricity sector as a whole, and renewables in particular, is a relatively recent phenomenon in the GCC.

The development of these capabilities calls for a new profession in the GCC: the energy policy and/or regulatory expert. This new role requires a continuous training and standardized formal certification and qualifications on a GCC or even pan-Arab level. Such experts would combine technical, financial, and industry knowledge and be able to make informed recommendations to policymakers based on robust energy models and in-depth scenario analyses. These professionals should also have a broad knowledge of the technical and business sides of all major sectors of the energy industry, as well as a background in energy and environmental economics.

Conclusion

The shift to renewable energy will eventually affect all six GCC member countries. Yet GCC governments can influence the timing and trajectory of this inevitable transition. Given the region’s fiscal challenges, there is no room for delay, indecision, or incoherence. GCC countries need to get on the path to optimal renewable energy infrastructure development in order to minimize costs while helping achieve their national economic development objectives.

1 The GCC countries are Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates.

Contact us

Menu